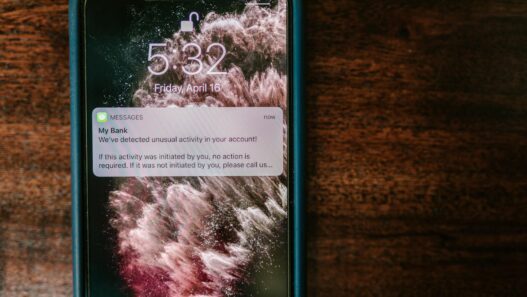

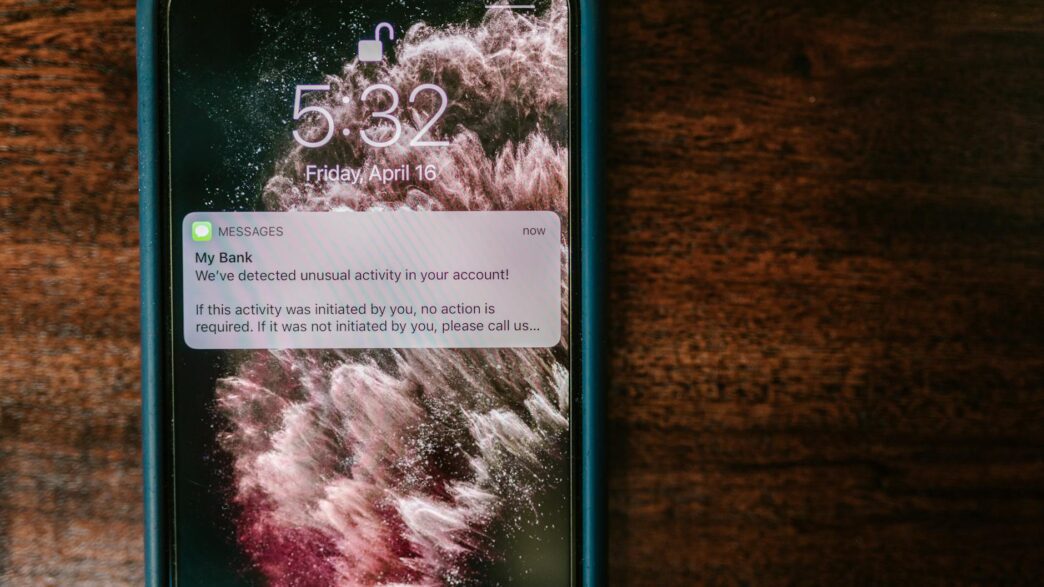

If your bank could send you a quick text right before you accidentally overdraft, would you read it? Of course you would. The wild part is that almost every checking account in the country already offers free alerts that can do exactly that, and most of us never bother turning them on. According to Citizens Bank, only about 55% of its customers have opted into account alerts, which means nearly half are walking around without the simplest, cheapest fraud-and-fee shield a bank gives away for free.

Bank alerts are quietly one of the highest-leverage moves a budget-conscious person can make. They take roughly five minutes to set up, cost zero dollars, and can save you hundreds of dollars a year in overdraft fees, missed-payment penalties, surprise subscription charges, and even fraud you never would have spotted in time. With the average overdraft fee still sitting at $26.77 according to Bankrate’s most recent Checking Account Survey, it only takes one or two avoided slip-ups for alerts to start paying for themselves many times over.

Here is the strategy I would use if I were starting from scratch this afternoon.

Start With the One Alert That Pays for Itself: Low Balance

The single highest-value alert you can set is the low balance trigger. You pick a dollar amount that feels uncomfortably close to zero — say, $200 if you usually float higher, or $50 if you run a tighter ship — and the bank pings you the moment your checking dips below it. That tiny notification is the difference between catching a problem on a Monday afternoon when you can move money and discovering it on Friday morning when three transactions have already cleared and you owe roughly eighty bucks in overdrafts.

Most people set this number too low. The whole point is to give yourself a buffer to react, so pick a threshold that goes off while you still have time to transfer from savings, delay a non-essential purchase, or rearrange a bill date. If you get the alert and immediately think “yeah, I knew that, I’m fine,” that is a win, not a false alarm. You want a system that nudges you a little too often rather than once too late.

If your bank lets you set two thresholds, even better — use one as a “look alive” warning at, say, $500, and a second emergency-level alert at $100. The first encourages course correction; the second forces it.

Layer in a Large Transaction Alert for Fraud and Sticker Shock

The second alert worth setting on day one is a large purchase notification. You decide what counts as “large” — $100 is a sensible default for most households, $50 if you live lean — and the bank texts you any time a debit or charge clears above that amount. This catches two very different problems at once.

The obvious one is fraud. The Consumer Financial Protection Bureau is clear that the faster you spot an unauthorized debit-card charge, the more legal protection you have and the easier the dispute. Spotting a $480 charge from a state you have never visited within minutes rather than days dramatically increases your odds of clean recovery.

The less obvious one is your own behavior. There is real data showing that when spending becomes invisible — tap to pay, autopay, in-app purchases — we underestimate it. A “you just spent $137” buzz on your phone forces you to consciously register what you did. That tiny moment of awareness is sometimes the only thing standing between a one-time splurge and a quietly expensive habit.

Catch Subscription Creep With Recurring-Charge and Direct-Debit Alerts

If your bank offers it, turn on alerts for any recurring debit or ACH withdrawal. This is the one that catches subscription bloat — the streaming service you forgot about, the gym you stopped attending in February, the SaaS tool whose free trial silently flipped into a $19 monthly charge. Federal Reserve research has found Americans systematically underestimate how much they spend on subscriptions, often by a factor of two or three.

A monthly $14.99 charge does not feel like a budget problem. Six of them do. Catching one of these as soon as it lands gives you a clean cancellation window before the next billing cycle. Pair it with the loose habit of asking yourself “did I actually use this last month?” every time the alert fires. Two cancellations a year easily covers the cost of a streaming service you actually want.

Set a Direct Deposit Confirmation Alert

This one feels boring until the day it isn’t. A direct deposit alert tells you the moment your paycheck (or government benefit, or refund) hits the account. On normal weeks it is a tiny dopamine hit. On the rare week when payroll messes up, your hours were misclocked, or HR forgot to process a raise, it is the warning shot that gets you to your manager before you bounce rent.

It is also genuinely useful for cash-flow planning. If you bank with an institution offering early direct deposit — many online banks and credit unions now release funds up to two business days early — knowing the exact moment money lands lets you time bill payments, transfers to savings, and bigger purchases without guesswork.

Don’t Skip the ATM and Card-Not-Present Alerts

Two more underrated triggers: ATM withdrawals over a chosen amount and any card-not-present transaction (online or phone purchase). The ATM one is fraud insurance — if a skimmer copies your card and someone pulls $400 from a machine in another state, you want to know immediately, not at the end of the month. The CFPB notes that the difference between reporting unauthorized debit-card use within two business days versus later can mean the difference between $50 of liability and up to $500.

The card-not-present alert catches the more modern version of fraud, where a stolen card number gets tested at small online merchants before a bigger purchase. A surprise $2.99 charge from a website you have never used is almost always a test transaction. Catching it lets you freeze the card before the real hit lands.

Add a Maintenance Fee Trigger If You Pay One

This one is sneakier. Some banks will alert you when you are at risk of triggering a monthly maintenance fee — usually because your direct deposit hasn’t arrived in the qualifying window or your average balance is trending below the minimum. If your bank offers this, turn it on. The whole point of those minimums is that the bank is hoping you forget. A nudge a few days before the cycle closes gives you a chance to deposit a few dollars, transfer in from savings, or rearrange a payroll splitter to keep the fee at zero.

If your account routinely fails the no-fee requirements, the alert is also a nice gut check that you are paying for the wrong checking account. Plenty of no-fee online checking options exist now with no minimum balance and no monthly fee, and switching is far less painful than it used to be.

How to Actually Set Them Up

In almost every banking app, alerts live under a settings menu called something like “Alerts,” “Notifications,” or “Manage Alerts.” You usually pick the trigger, the threshold, and the delivery channel — text message, push notification, email, or some combination. Push notifications are usually fastest. Text is best if you keep notifications muted. Email is fine for low-priority items like statement availability but is too slow for fraud alerts.

A reasonable starter set: low balance push, large transaction text, recurring debit email, direct deposit push, ATM withdrawal text, card-not-present text, and maintenance fee push. Spend ten minutes doing it once and you have built a free, always-on layer of friction between your money and the people, fees, and habits trying to nibble it away.

The Bigger Picture

Alerts are not exciting. They will not earn you 4.5% APY or shave a couple hundred basis points off your mortgage. What they do is dramatically reduce the percentage of your money that disappears into preventable mistakes — the overdrafts, the unnoticed fraud, the autopay you forgot to cancel, the maintenance fee you triggered by accident. For most people, those leaks add up to far more per year than the rate difference between a decent savings account and an excellent one.

If you remember nothing else from this article, do this today: open your banking app, find the alerts section, and turn on a low balance alert and a large transaction alert. Five minutes, zero dollars, and probably the highest-ROI personal finance move you will make all week.