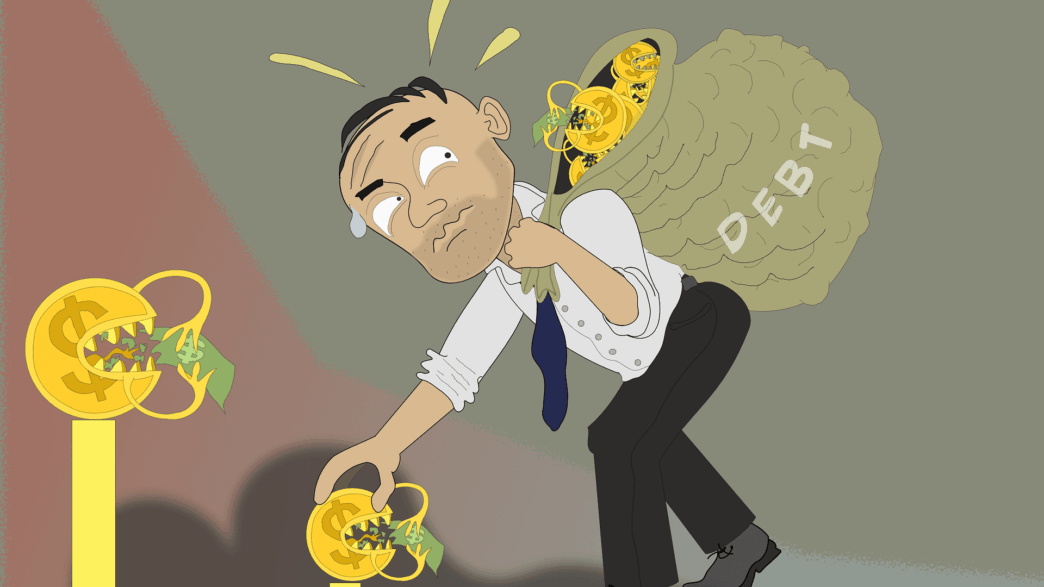

You can do a number of things to eliminate debt entirely, or at least pay off most of it. Being in debt can be stressful for anyone, regardless of your circumstances or the amount you might owe to another party.

Here are 5 steps you should take, which will help cut down your debt levels.

Step 1: Estimate Your Financial Obligations

As a first step, you need to know how much you owe and to whom. It’s a salient idea to organize your figures on an excel sheet or use an online debt calculator to keep a tab of kind of debt (loans, credit card), interest rates (in order of lowest to highest), and the total amount due to various parties.

You will never hit your target to mitigate debt if you don’t know how much it really is. Be upfront about it and create a systematic debt reduction plan that will actually work.

You should also prepare a list of your monthly income and expenditure while you are computing your total debt. Expense items would typically be listed on your credit cards and you can take account of the cash expenditures from your bank statements.

This will provide you with a fair picture of the total debt and how much you might be able to spare every month to pay off the most expensive debt components first.

Step 2: Halt any Further Debt Creation

You need to stop creating more debt if you plan to reduce it. You will never be able to get out of the vicious debt trap if you continue using borrowed money to finance your lifestyle. Remember, you are not the state of California or Congress.

For instance, you can curb the habit of charging some credit cards to pay off the debt amount on others.

Get into the habit of utilizing cash as your primary mode of payment. This will at least start reducing your credit card interest costs, and even deter you from making impulsive purchases. It is far easier to spend money by paying with plastic on things you do not need.

Postpone any non-essential purchases, and start focusing exclusively on resolving your current debt situation.

Step 3: Have a Prudent Debt Elimination Strategy in Place

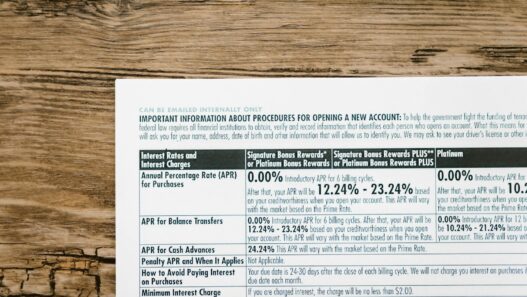

Your goal should be to double down on your credit card payments because credit cards usually have the highest interest charges which is no fun to pay even during a solid economy with lower taxes. Unless you create a solid debt management strategy and execute it with a firm resolve, it will be difficult to come out of the debt cycle.

Snowball Debt Reduction Approach

This strategy involves paying off your smallest debts first. The advantage is that when you start small, it will give you the confidence that you can come out of your situation one small step at a time. The emotional advantage will be immense when you see your smaller loans are getting eliminated one by one.

Once you begin small, you will continue to gather momentum to take more tangible debt reduction steps. One small step will eventually ‘snowball’ into a huge dedicated endeavor on your part to eliminating your bigger debts.

Avalanche Debt Reduction Approach

The avalanche debt management strategy involves paying off the costliest debt first. Remember that your goal here is to focus on the highest interest rate, and not the total debt amount or the total interest cost.

While you can keep paying minimums on other debts, you can start working on eliminating those debts first which are crushing you with a very high interest burden.

Stay committed to the debt reduction strategy you choose, and slowly you will start emerging out of your difficult debt situation.

Step 4: Set Aside an Emergency Fund

While it may appear counter-intuitive to set aside an emergency fund when you are working to eliminate debts, this is a vital step that will help you prevent additional debt. Life offers no guarantees to support you in your difficult financial situation.

An unforeseen health trouble, car breakdown, or a leaky roof needs to be taken care of, and if you have an emergency fund, you will not be forced to pile on more debt. Keep a goal of building a fund of about $1,000 for these types of emergencies.

Step 5: Consolidate Multiple Debts into a Single Loan

A well-structured debt consolidation plan can help you combine multiple consumer debts into a single loan. This will usually result in a lower overall interest rate on the entire amount, and you will need to make just one payment every month.

It will simplify your finances, and give you clear goals about debt elimination. You will have to discuss with your credit union, bank, or another lender to see if they are willing to cooperate with you on this proposal of debt consolidation.